Since the market has just “delivered” us an episode of great volatility concentrated, at least for now, in a few days, we believe it might be nice to contextualize it by going back in time. Not so much to understand whether it is over or not, which as we well know is impossible to do, but to show you curious episodes.

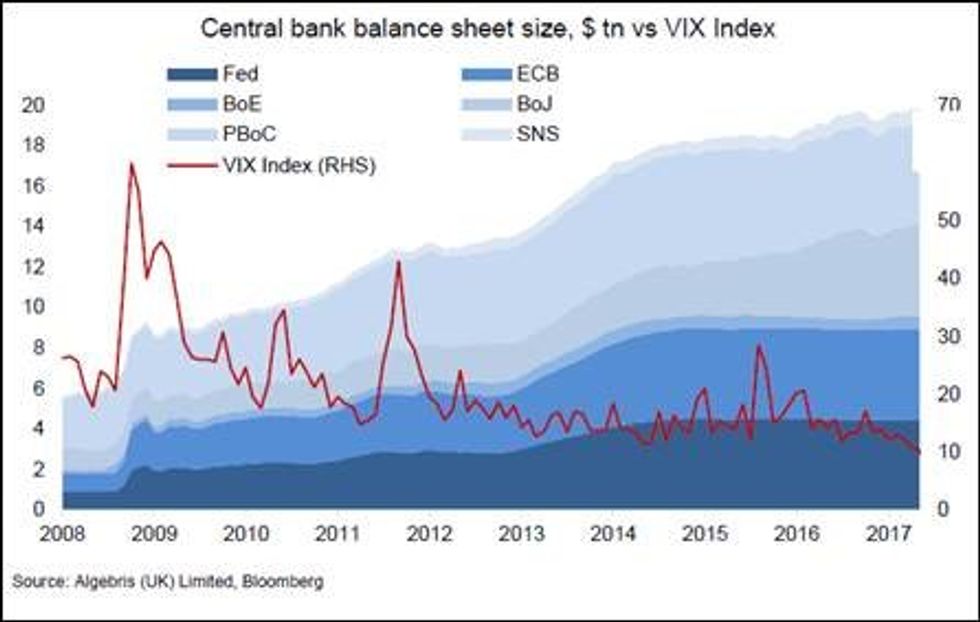

First of all, it must be said that after the great financial crisis we have experienced a period in which there have been few episodes of volatility with central banks in the field with their quantitative easing acting as “guardians” of the markets. The Algebris graph shows us precisely how the volatility of the American stock market (VIX index for technicians, in red), a parameter often taken as a reference, has fallen sharply in the period 2009 – 2017. This phenomenon went hand in hand with the increase in the balance sheets of the central banks of developed countries, with the drop in rates to negative values (how absurd to see it today ex post) and with the desire to “keep calm on the markets” and continued for a good 12 years until February 2020.

This historical phase ended with the Covid shock that brought a lot of volatility to the markets (spring 2020) and then with the normalization of rates (2021-2023) that brought the rules of the game back to more appropriate methods. The only aberration still in progress is the lack of term premium on the bond side (flat or inverted yield curves), but here too the markets are working on it.

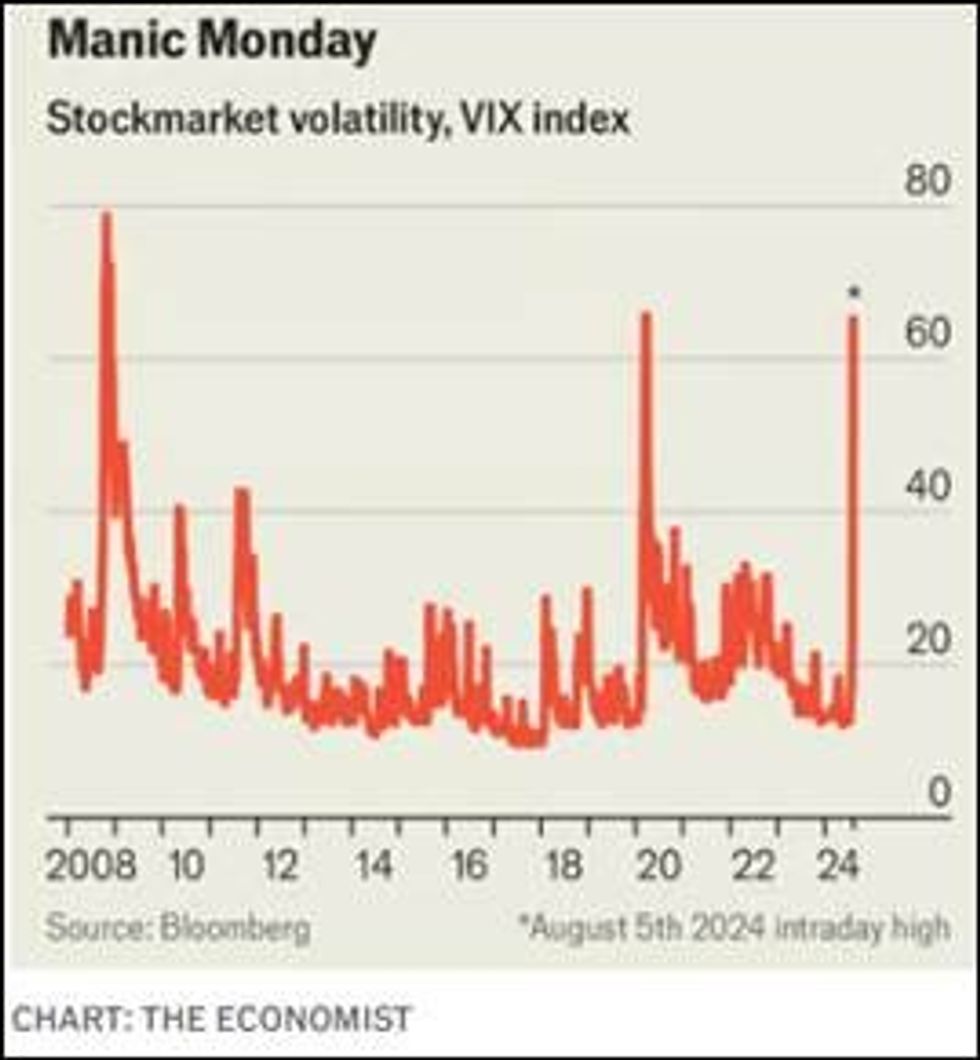

So episodes of volatility could return to be more frequent and perhaps even faster. For the record, the VIX reached an intraday value in the 55 area in the recent episode, lower only than the Covid peaks (60) and the great financial crisis (almost 80) as the Bloomberg / The Economist graph shows us. The speed of the climb is what surprised us the most given that we were not facing a pandemic, nor the greatest risk faced by the financial system since the Second World War. Probably markets increasingly driven in the short term by algorithms and computers, the development of AI and little liquidity present are the most logical explanations we can give today.

What episodes of volatility from the past can we tell you about? Using the Bloomberg graph (normalized volatilities of the last 20 years) we see that there is not only the volatility of the stock markets, but each asset class has its own, just measure it. We observe that the peak of highest volatility belongs to oil which in April 2020 exploded when the price of oil became negative, falling to -40 USD per barrel in the United States; do you remember? The world stopped due to Covid, ships full of crude oil parked with no one who wanted to accept deliveries, people willing to pay to sell oil, a rare and unique event.

We can then remember 2008, the year in which currency volatility reached very high levels, to be clear, equal to 3 times the current values that remain very low (the most important currency pair Euro/US Dollar has been in a very narrow lateral channel for 18 months now). To remember what happened then, let’s talk about the Japanese Yen, much cited these days as a contributory cause of the volatility seen on the markets, which went in less than 6 months from levels equal to 170 Yen per Euro up to 115 with an appreciation close to 50%. Today the movement has been around 10% and therefore much more limited.

Finally, we bring to mind one last episode of volatility and return to stocks: on October 19, 1987, a Monday, now known to all as “Black Monday,” the Dow Jones fell by 22.61% in a single day, a record that still stands today. After reaching its all-time highs on August 25, the American stock market began to fall, arriving on the fateful day already down by about 12%; on that black day there was real panic and the FED had to intervene the next day by injecting enormous amounts of liquidity into the financial system. As you can see, something very similar to what still happens today. For the record, the month of October 1987 ended badly not only for the American stock market, but for all those of other countries with drops of over 40% for Australia, Singapore and Hong Kong.