Let's continue the analysis of this unusual phenomenon of the net supply of shares which has become negative after having seen last time how the “new share listing” component has been very low in the past two years.

The other two elements that influence this strange result are the delisting of shares from the stock exchanges, typically through a takeover bid and subsequent cancellation of the company's listing from the list, making it “private”, and share buyback operations, through which listed companies own shares are bought back on the market.

Even in 2024 we have already seen several takeover bids or “takeovers” as they say in Anglo-Saxon jargon: think of the very recent “hostile approach” of the Spanish bank BBVA towards its fellow countryman Banco de Sabadell, of Lavazza's takeover bids for IVS Group and of the French companies such as LVMH on Tod's in our country or those of private equity on Salcef Group in Italy or on Paramount in the United States, just to name a few.

The result is that the number of companies listed on the stock exchange has been decreasing for years. And not by little, look at the graphs that Schroders shows us (updated at the end of 2022):

Real collapse in the United Kingdom with 3 out of 4 companies disappearing in 60 years, also a decline in Germany from the post-internet bubble peaks of the 1998-2001 period (during which many “.com” companies were listed on the German technology Neuer Markt) , a significant decline also in the United States (-50% from the highs) with a good final recovery thanks to the many prices of 2021.

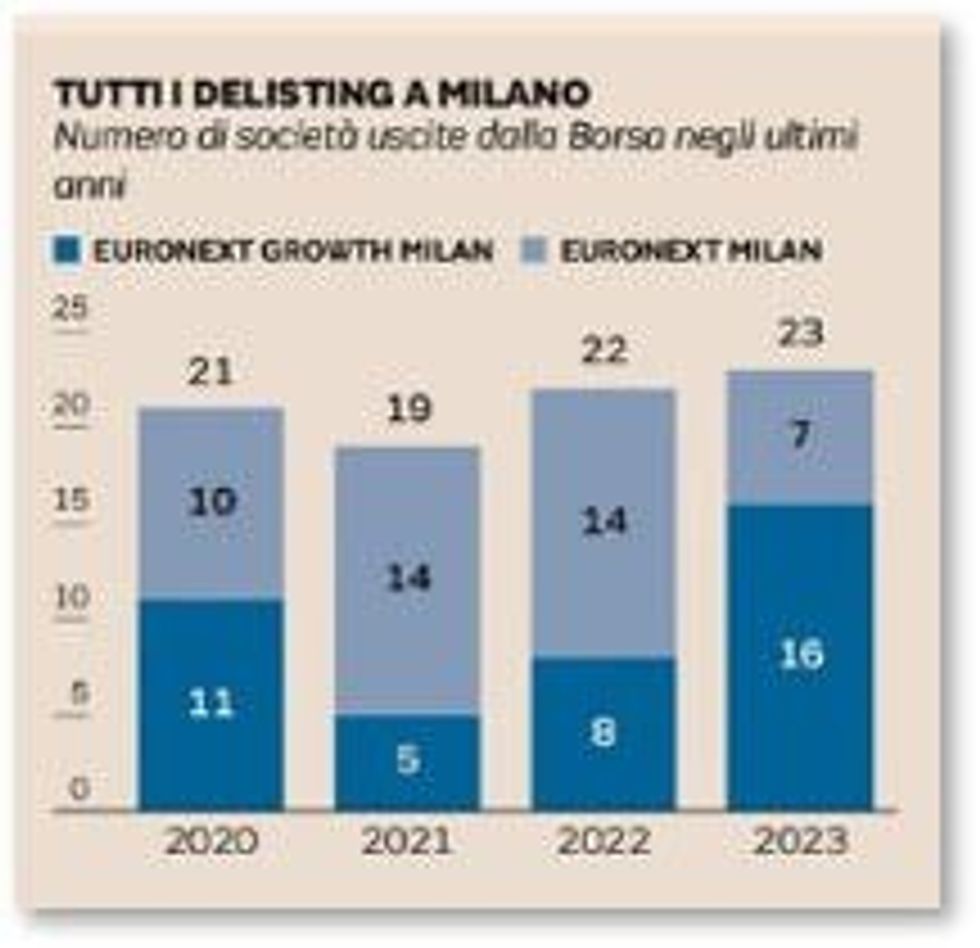

And what's happening on the Italian Stock Exchange? Things are better! There are always exits from the list (as you can see from the Il Sole 24 Ore graph, about twenty per year on average), but there is also, in contrast with many other world markets, a growth in IPOs.

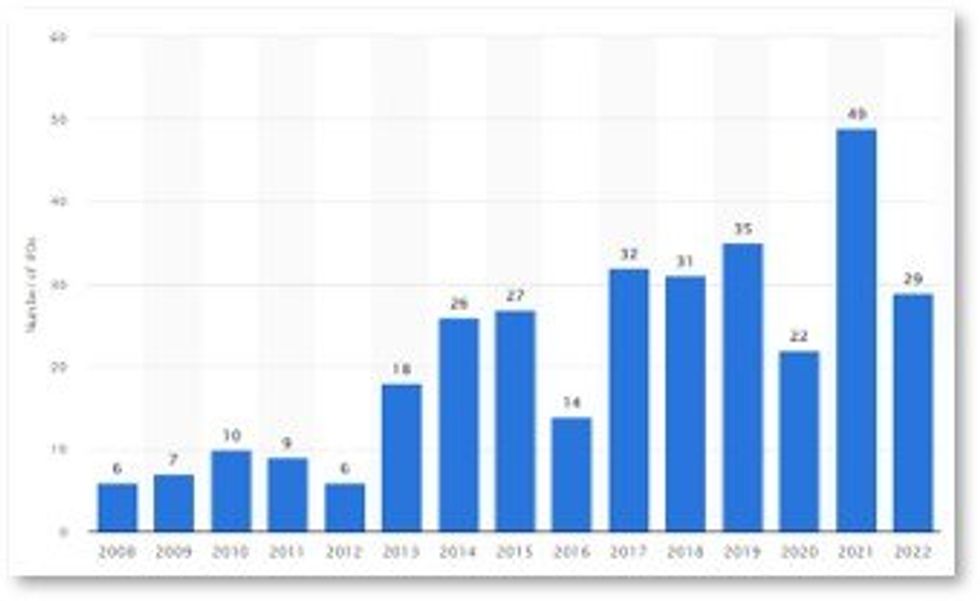

The Statista graph shows it and the missing number (for 2023) is an excellent 36 with many small and medium-sized companies that have gone public, also thanks to the excellent work done by our stock exchange, part of the Euronext group.

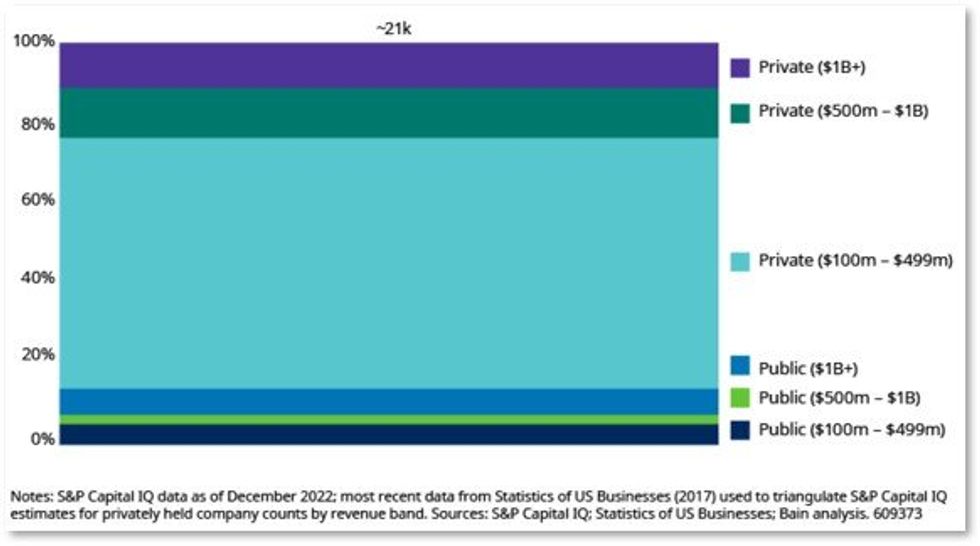

If we broaden the analysis we realize that the fact that a company being listed is not such a common thing around the world. Apollo shows us how in the USA only 13% of companies with a turnover above 100 million dollars are listed, while all the rest are not.

In Europe the figure is even clearer, and it is normal that this is the case given the lower strength of the capital markets: 4% versus 96%.

The world is “dominated” by unlisted companies so as the image of S&P Capital-Bain shows us well:

In short, the trend of the delisting factor seems clear and in the absence of a return of a more favorable window for new listings we can expect that the number of companies present on the stock exchange may decline further.

The new record was set once again by Apple with $110 billion announced just this month of May.

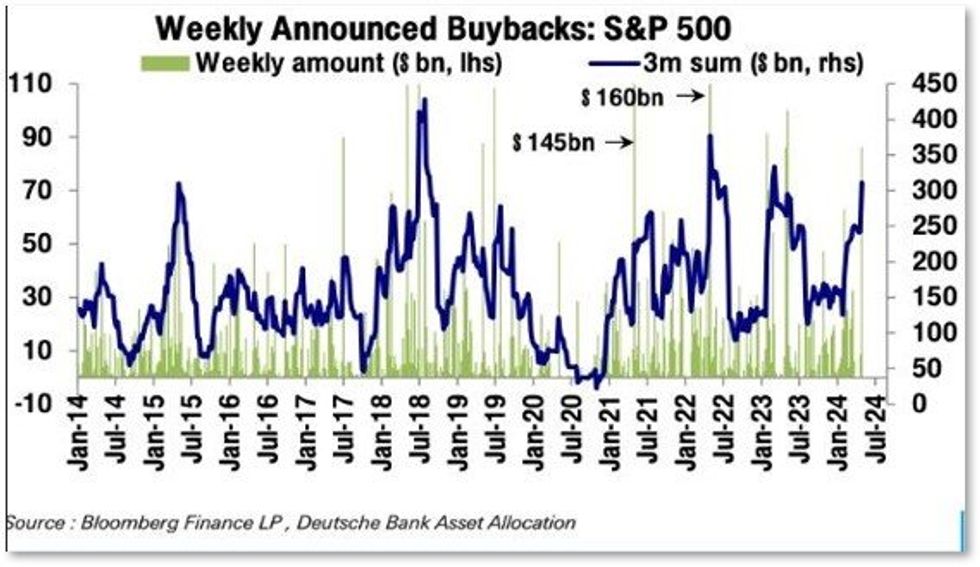

Buyback announcements are rather volatile as the Deutsche Bank graph shows us well, but apart from the first months of Covid, they are always very present. Moving on to the last element of our analysis, i.e. buybacks, we can highlight how the trend is very strong from several years now.

If we focus on the American market we can observe how all the largest share buyback operations have been carried out in the past five years with the infotech giants leading the way.

The new record was set once again by Apple with $110 billion announced just this month of May.

Buyback announcements are rather volatile as the Deutsche Bank graph shows us well, but the first months of Covid aside, they are always very present.

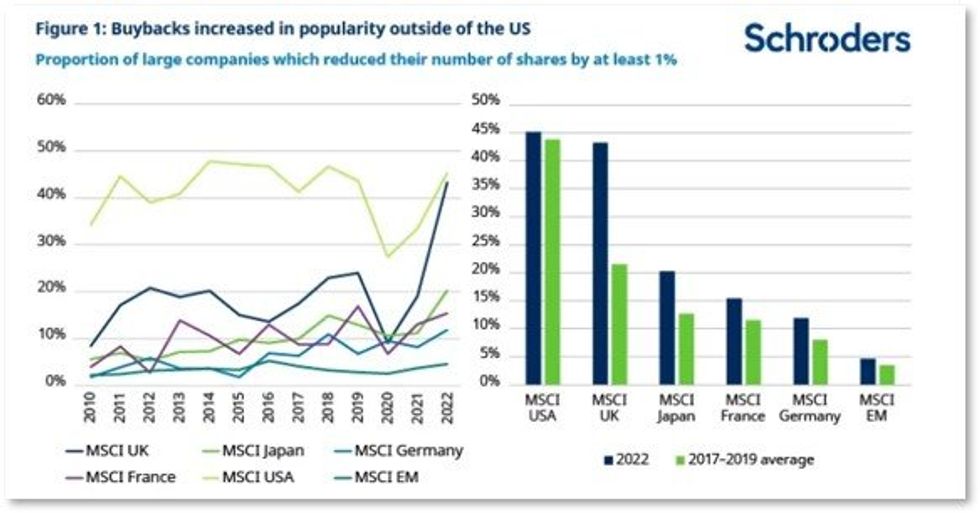

To understand in which other countries buybacks are popular, we are further helped by an excellent analysis by Schroders which shows how the percentage of companies that carry out buybacks and then cancel the shares is increasing almost everywhere in the world. In particular, English and Japanese companies are the main protagonists of an increase in these operations. We are not too surprised given that the UK market is typically value and has seen the prices of many companies lag behind the rest of the world markets despite good results and has therefore pushed shareholders and CEOs to implement buybacks.

In Japan the story appears even more interesting with, finally, many companies that have decided to reduce their enormous and historic cash reserves and use them for more productive uses including share buybacks.

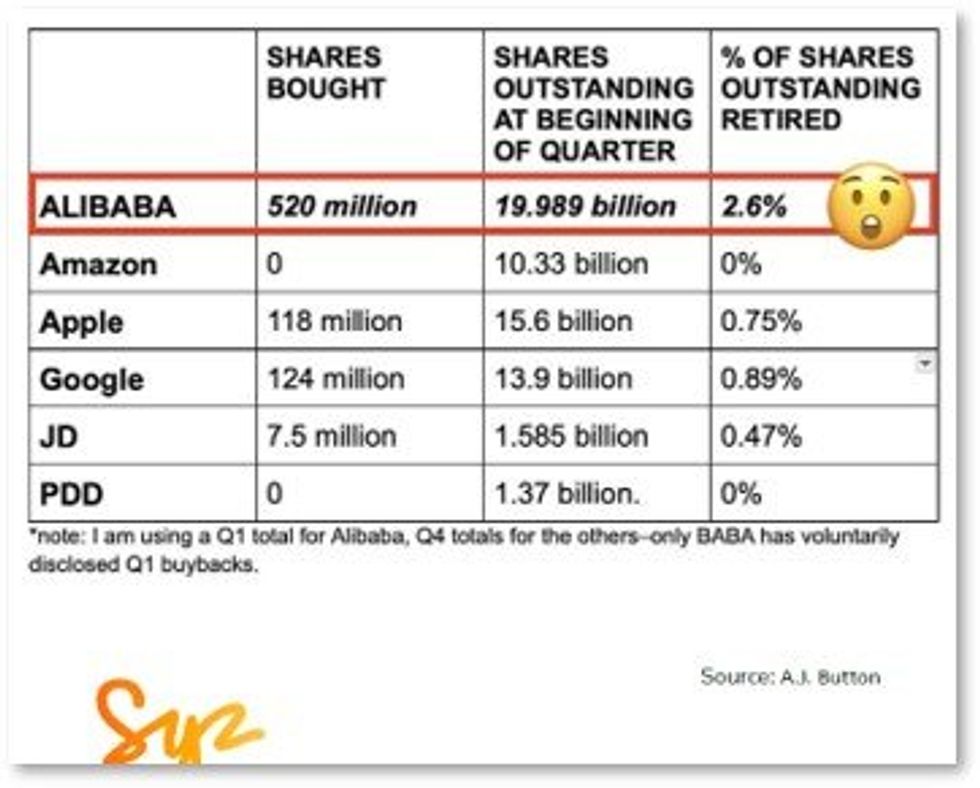

But the largest buyback taking place at the moment (Button-Banque Syz data) is not in the countries mentioned so far but in China where Alibaba has already bought back 2.6% of the total existing shares and, completing the announced purchase plan, will arrive to 4%. A record for a megacap and an excellent sign for those who believe in the recovery of Chinese shares, which Alibaba itself undoubtedly believes in.

The next edition of the column will see a drastic change of topic: we will talk about investments and sustainability.