Our cousins across the Alps are going through a rather turbulent moment on a political level and a complicated one on an economic level; our first reaction as Italians is to smile, also because Germany, for 20 years the panzer of the European economy, is also in a bit of a crisis. In short, the duo that ruled and continues to rule in the Eurozone, that made us see the green light in the times of the euro crisis and the excess debt, that imposed on us strict diets, reforms, budget constraints, that threatened to send us the Troika, is now moving in slow motion (France a +1% GDP growth this year, Germany even in recession) with problems at government level that are much worse than ours.

But let’s stick to the cousins. At a political level the country is divided and is unable to form a new government, Macron resists but is contested by many parties, citizens express a very low level of trust in the institutions. The image below shows us, in this sense, the rainbow of colors that is France after the last legislative elections.

Banca Patrimoni Sella & C.

At an economic level, serious problems have come to light in our opinion, which we summarize here:

- France is the country at Eurozone level that has most times broken the rule of a maximum of 3% annual deficit compared to GDP (20 times from 1999 to today compared to 18 in Greece or 14 in Italy).

- The problem was relative as long as the country’s Debt/GDP ratio was low (but today the situation has changed given that France with 112% is the third worst country in the Eurozone) and as long as the country was growing well (but here too there is has been a notable decline in recent years).

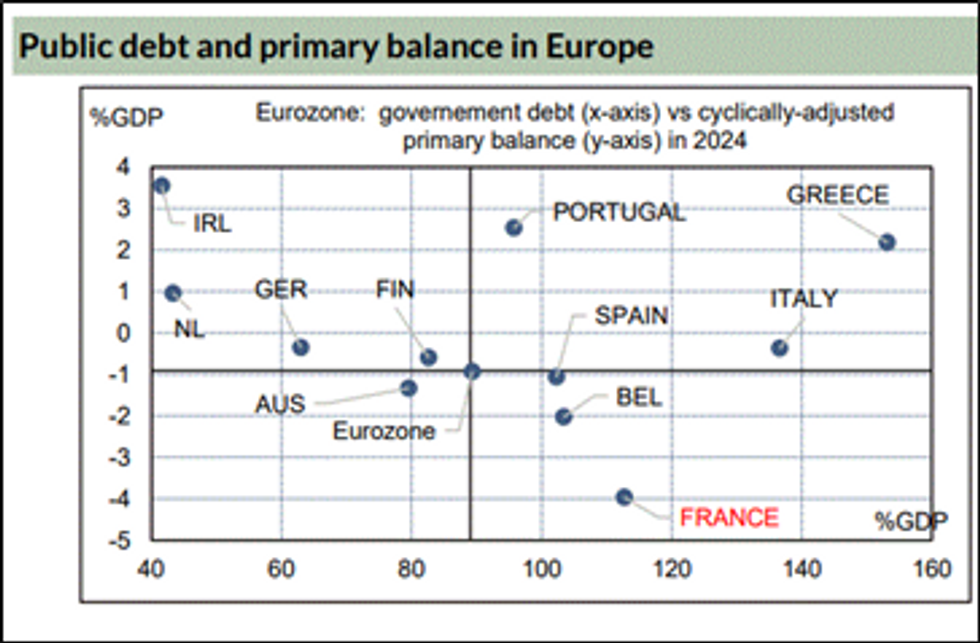

- Unlike Greece, Italy, Portugal, which are also in debt, but which operate with positive primary balances (from 1 to 3% of GDP in 2024), France is typically in negative (4% deficit compared to GDP this year ). The primary balance represents the air that a country has available to “breathe”, being the difference between state revenues and expenses (excluding interest).

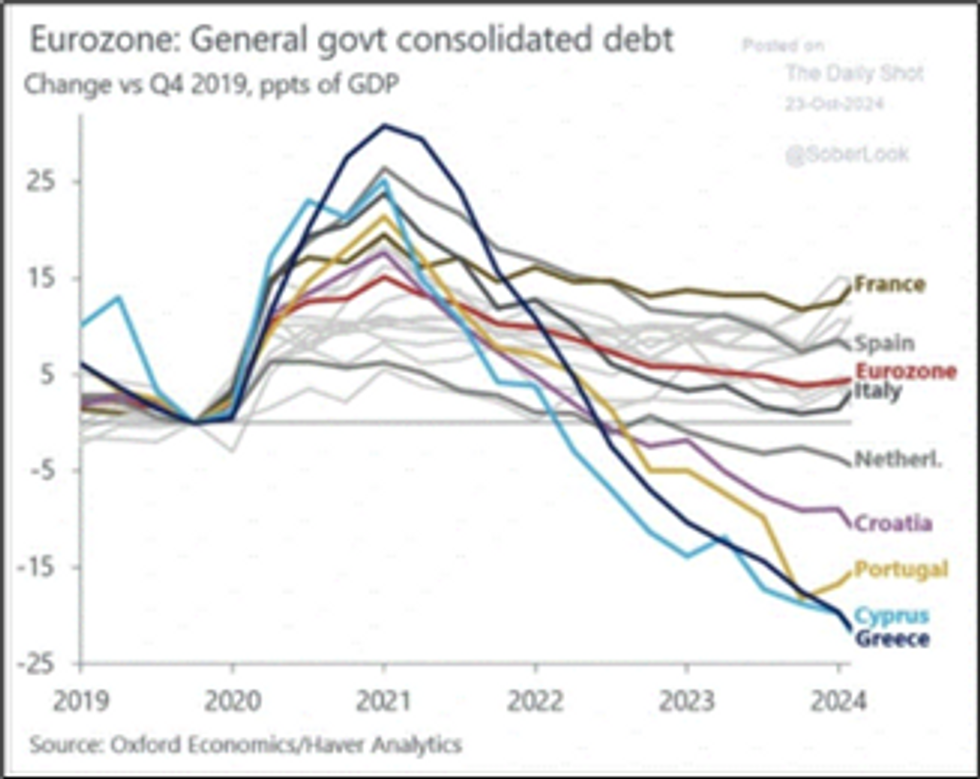

This last aspect is particularly critical and the Oddo BHF graph shows us well how transalpines live in oxygen debt.

And precisely this last aspect has determined in the last 5 years a huge delta between France (the worst) and countries like Greece or Portugal (with strong growth, which have managed the post-Covid period very well) in terms of debt/GDP delta . France rose by 15 percentage points, Greece fell by 20, Portugal by 15. The graphic image from Oxford Economics is very explicit.

It would therefore be time for rigorous policies, spending cuts and increased taxation to provide more revenue to the state. Well in France, a country extremely rich in social conflict, highly unionized, in which there are organizations that defend everyone’s interests and are ready to strike at the first sign of a reduction in historical privileges, it is practically impossible to carry out initiatives like “Mario Monti 2011 -2013”. I experienced all of this first hand in the 4 years I spent across the Alps.

The Barnier government fell after less than three months because no party wanted to approve the proposed budget. We were talking about 40 billion euros in cuts and 20 billion in additional taxes, a postponement of the retirement age by just 6 months, trifles compared to Monti’s measures or even more so the Fornero reform (Santa immediately for what he did).

The financial markets have only partially been affected by the situation (French stock market index CAC40 will underperform European equity by 10% in 2024, French government bonds today pay similar interest to Greek ones and much more than those of Spain or Portugal), but perhaps they underestimate the difficulty that France will still have to face to get out of this situation.

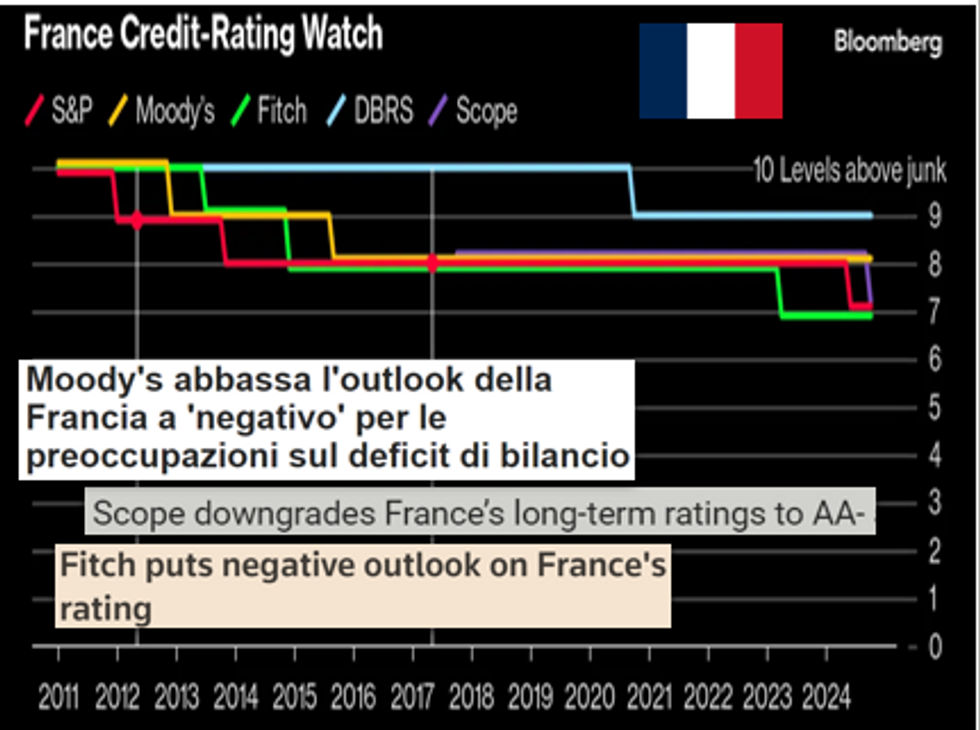

The rating agencies seem to understand this and have in fact lowered the creditworthiness of government debt, which to date remains higher than ours, and maintain a negative outlook.

A topic that will therefore remain, in my opinion, of great relevance also in 2025.