The first 4 months of 2024 have faced us with an anomalous and in some ways astonishing figure: the net supply of shares/companies on the world stock exchanges was negative by almost 150 billion dollars. But what does “negative” mean? It means that if from the few listings of new companies that have occurred on the various stock exchanges (IPOs and capital increases) we subtract the delistings (i.e. the cases in which a listed company goes back to being “private” through a takeover bid), and the corporate buyback operations in which a company buys its shares on the market (often to then cancel them) we obtain a negative figure. It is as if the large pool of listed companies in the world was partially drying up.

The graph offered to us by the Financial Times shows us the anomaly of such a situation; a negative figure of a magnitude similar to that of this first quarter of 2024 had never been seen in the last 25 years.

(Financial Times)

Normally, on a global level, the stock exchanges offer an average of 400 – 500 billion in net supply of equity capital per year which investors have always calmly absorbed. Even recently, excellent years such as 2020 and 2021 have been recorded with values close to 700 billion; it is true that over time the trend is downward given that the records of the late 1990s have never been seen again, but the 2024 data and also that of 2023 (also negative with -40 billion) pose important questions.

So let's try to understand the reason for this phenomenon. Today we will focus on IPOs, while in the next episode we will talk about the delisting element and the buybacks element.

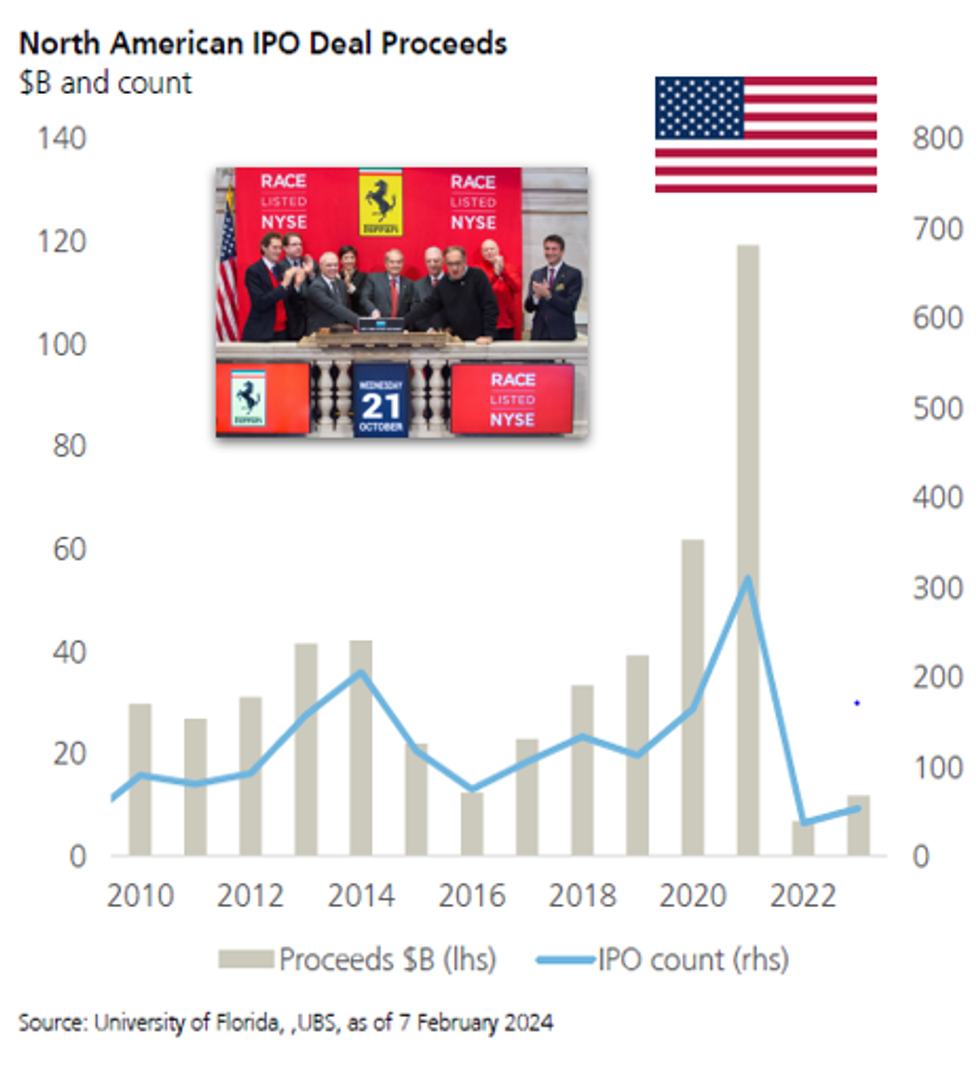

First of all, new company listings on the stock exchange are at their lowest levels in the last twenty years ($50 billion in value in the USA and only €12.5 billion in Europe in 2023). 2024 also got off to a slow start on both continents. It is very difficult to get to the end of a listing process, there have been dozens of IPOs announced and then withdrawn due to lack of investor interest. The UBS graph shows us how in the United States the collapse since 2021 has been truly impressive both in terms of number and value of transactions. In short, the days of Ferrari-style IPOs are long gone.

One of the main reasons for the current situation is undoubtedly the high level of interest rates which makes it more complex to make the valorization of a new registration attractive compared to the years of low or even negative rates. Then the current strong sectoral concentration of market indices and investment flows greatly limits the areas and businesses that the market and investors deem attractive today.

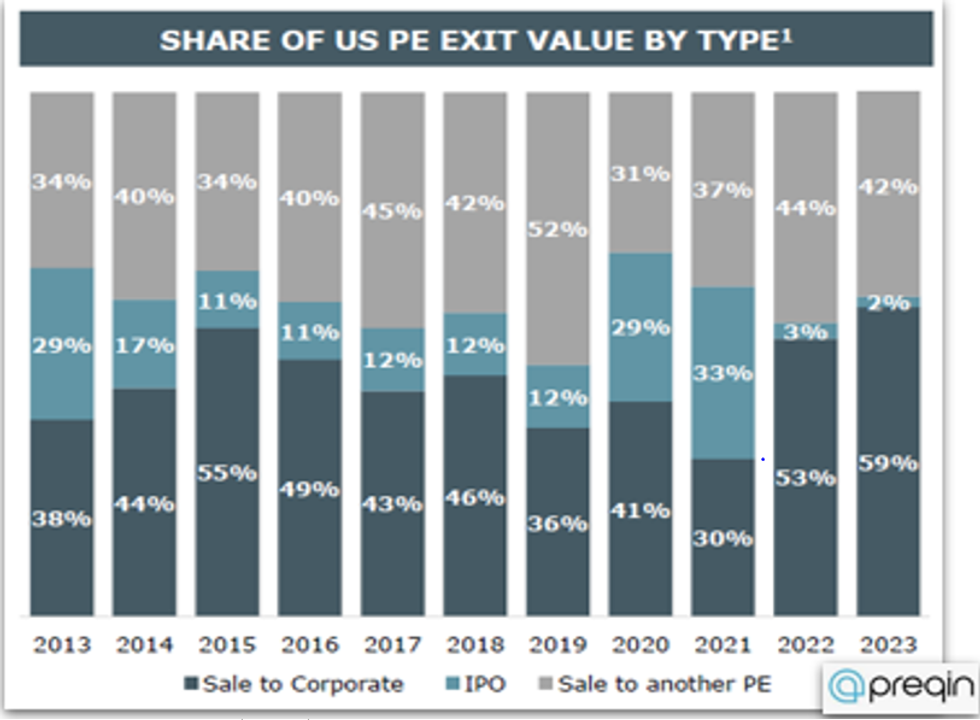

To make it clear how difficult it is to list new companies, it is enough to observe how on the private equity fund side, the percentage of company sales that take place through the IPOs channel has fallen to an all-time low with only 2% of the total compared to historical averages which typically they fluctuated between 15 and 30%. Here perhaps even high load ratings can be a problem. Prequin's graph requires no further comment.

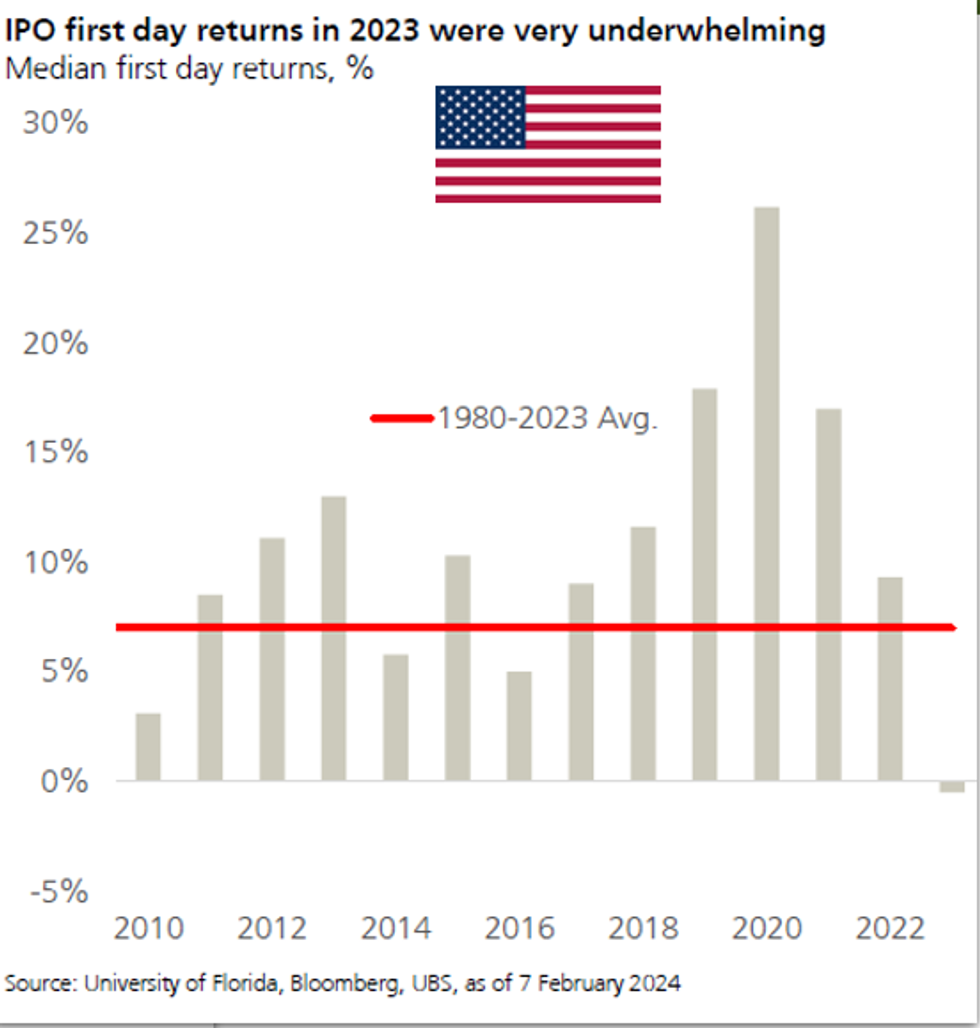

A clear signal of the low demand is offered by the index which measures the performance of the first day of listing of a “newbie” on the stock exchange. We can see how far away are the days when the average figure reached 20-25% with investors snatching IPOs out of their hands. Here too, 2023 recorded the worst data ever with an eloquent -1%.